Understanding the Basics of a Home Equity Line of Credit

If you are a homeowner in Dunedin, FL, looking to fund a major renovation, consolidate debt, or cover unexpected expenses, a HELOC home equity line of credit might be the perfect financial tool. A Home Equity Line of Credit, also known as a HELOC, allows you to borrow against the equity you have built up in your property. Unlike a traditional lump sum loan, a HELOC functions much like a credit card, giving you the flexibility to draw funds as you need them and only pay interest on the amount you actually use.

At Mortgage Info by Sean, we specialize in helping Florida homeowners navigate their financing options. Whether you are exploring a home equity loan or second mortgage, or you are considering a cash-out refinance, our team is here to guide you. We are also experts at providing second opinions on HELOCs, ensuring you get the best possible terms for your unique financial situation.

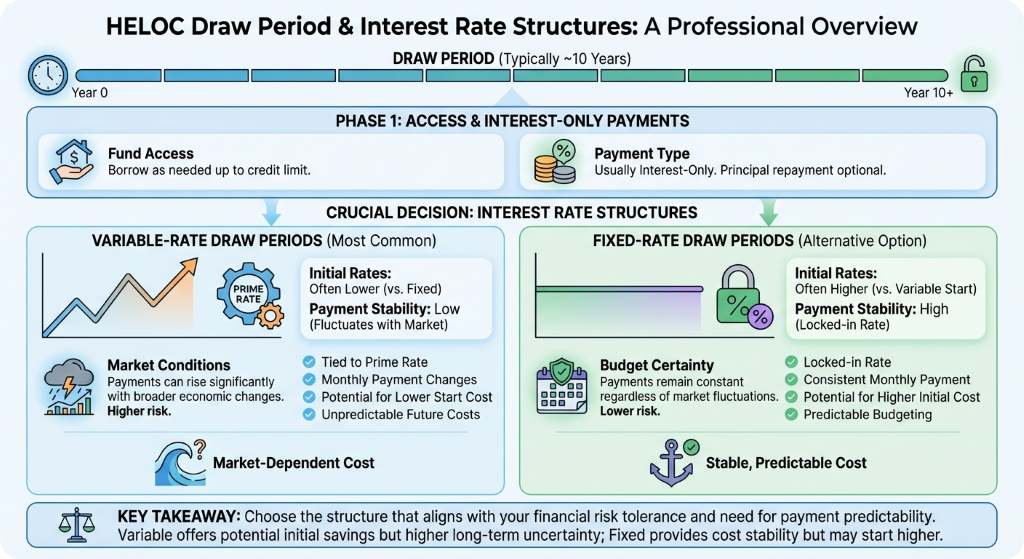

Variable-Rate vs. Fixed-Rate Draw Periods

When you open a HELOC, you enter what is known as the draw period, which typically lasts around 10 years. During this time, you can access your funds and usually make interest-only payments. It is crucial to understand the difference between the interest rate structures available during this phase.

- Variable-Rate Draw Periods: Most HELOCs start with a variable interest rate tied to the prime rate. This means your monthly payments can fluctuate based on broader market conditions. While initial rates might be lower, there is a risk of your payments increasing over time.

- Fixed-Rate Draw Periods: Some lenders offer the option to lock in a portion or all of your balance at a fixed interest rate. This provides predictable monthly payments and protects you from rising market rates, making it easier to budget for your household.

Choosing between a variable and fixed rate depends heavily on your financial goals and market trends. As your trusted mortgage loan consultant in Dunedin, Sean McManamon can help you analyze these options to find the most secure path forward.

| Feature | Variable-Rate HELOC | Fixed-Rate HELOC Option | Cash-Out Refinance |

|---|---|---|---|

| Interest Rate Structure | Fluctuates with the market | Locked rate for a specified balance | Fixed or variable for the entire new loan |

| Payment Predictability | Low | High | High (if fixed) |

| Fund Access | Revolving credit line | Revolving credit line | Lump sum payout |

| Best For | Ongoing, unpredictable expenses | Budgeting for specific large expenses | Securing a lower rate on a primary mortgage |

Why Get a Second Opinion on Your HELOC?

Securing a HELOC home equity line of credit is a major financial decision. Even if you already have an offer from your primary bank, getting a second opinion can save you thousands of dollars in interest and hidden fees. Lenders structure their margins, caps, and introductory rates differently.

We are experts at providing second opinions on HELOCs. By reviewing your current pre-approval or loan estimate, we can identify potential red flags and uncover better opportunities. Our deep understanding of the Dunedin real estate market allows us to offer tailored advice that national lenders often overlook. Do not settle for the first offer you receive; let us ensure you are maximizing the potential of your home equity.

Q1: What exactly is a HELOC home equity line of credit?

A HELOC is a revolving line of credit that uses your home as collateral. You can draw funds as needed up to a certain limit and only pay interest on the amount you borrow.

Q2: How does the draw period work on a HELOC?

The draw period is the initial phase of the loan, usually lasting 10 years. During this time, you can access your funds and are typically only required to make minimum interest payments.

Q3: Can I switch from a variable rate to a fixed rate on my HELOC?

Yes, many modern HELOCs offer a fixed-rate option that allows you to lock in a specific interest rate on a portion or all of your outstanding balance during the draw period.

Q4: How is a HELOC different from a home equity loan?

While a HELOC provides a revolving line of credit with variable or fixed-rate options, a home equity loan gives you a single lump sum upfront with a fixed interest rate and fixed monthly payments.

Q5: Why should I get a second opinion on my HELOC offer in Dunedin, FL?

Different lenders offer varying margins, rates, and fee structures. Getting a second opinion from a local expert ensures you receive the most competitive terms and avoid unnecessary costs.