What is an Adjustable-Rate Mortgage (ARM)?

An Adjustable-Rate Mortgage (ARM) is a home loan with an interest rate that can change periodically. This means your monthly payments may go up or down based on market conditions. Unlike a traditional 30-year fixed-rate mortgage or a 15-year fixed-rate mortgage, an ARM typically offers a lower initial interest rate for a set period. After that introductory period ends, the rate adjusts at specific intervals. If you are looking for a lower initial payment to afford your dream home in Dunedin, FL, an adjustable rate mortgage might be the perfect solution. Sean McManamon and the team are experts at providing second opinions on adjustable-rate mortgages to ensure you are getting the best terms possible.

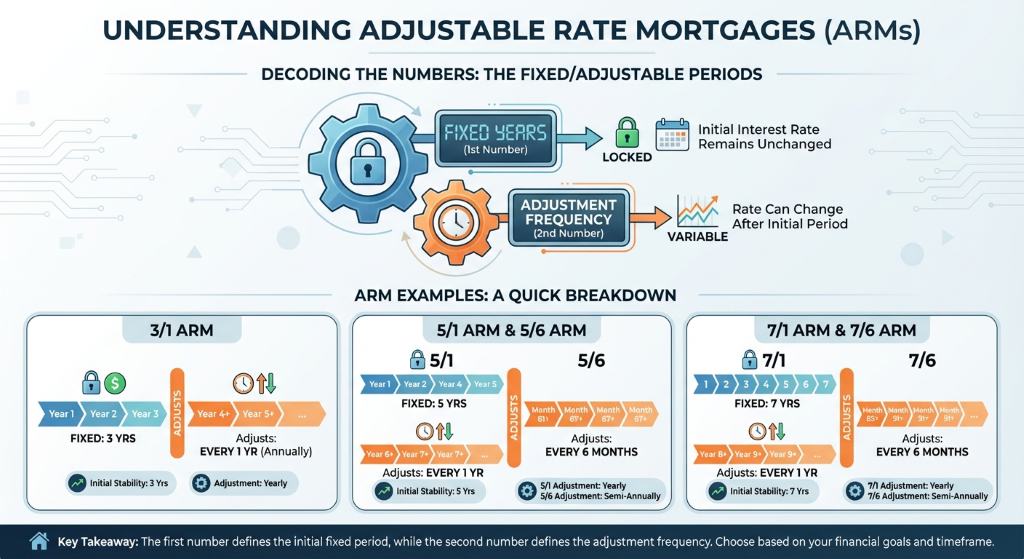

Understanding ARM Terms: 5/1, 7/1, 5/6, and More

When exploring an adjustable rate mortgage, you will notice numbers like 5/1, 7/1, or 5/6. The first number represents the number of years the initial interest rate remains fixed. The second number indicates how often the rate can adjust after that initial period. Here is a quick breakdown:

- 3/1 ARM: Fixed for 3 years, adjusts once every year thereafter.

- 5/1 ARM and 5/6 ARM: Fixed for 5 years. A 5/1 adjusts yearly, while a 5/6 adjusts every six months.

- 7/1 ARM and 7/6 ARM: Fixed for 7 years, adjusting yearly or every six months respectively.

- 10/1 ARM: Fixed for 10 years, adjusting annually afterward.

These structures are available for standard loans as well as a jumbo mortgage. Understanding these terms helps you align your home financing with your future financial goals. If you ever want to lock in a permanent rate later, you can always explore a rate-and-term refinance.

| ARM Type | Fixed Period (Years) | Adjustment Frequency |

|---|---|---|

| 3/1 ARM | 3 | Annually |

| 5/1 ARM | 5 | Annually |

| 5/6 ARM | 5 | Every 6 Months |

| 7/1 ARM | 7 | Annually |

| 7/6 ARM | 7 | Every 6 Months |

| 10/1 ARM | 10 | Annually |

Protecting Your Investment: Caps and Floors

One of the biggest concerns borrowers have with an adjustable rate mortgage is the fear of skyrocketing payments. Fortunately, ARMs come with built-in protections known as caps and floors. These limits dictate exactly how much your interest rate can change.

- Initial Adjustment Cap: Limits how much the interest rate can increase the very first time it adjusts.

- Subsequent Adjustment Cap: Caps the amount the rate can increase during each subsequent adjustment period.

- Lifetime Cap: The absolute maximum interest rate you will ever pay over the life of the loan.

- Interest Rate Floor: The lowest possible rate your mortgage can drop to, protecting the lender.

As Dunedin local mortgage experts, we specialize in providing second opinions on adjustable-rate mortgages. We will review the caps and floors of any offer to ensure you are fully protected.

Q1: What is an adjustable rate mortgage?

An adjustable rate mortgage is a home loan where the interest rate remains fixed for an initial period and then adjusts periodically based on market indexes.

Q2: Is a 5/1 ARM a good idea?

A 5/1 ARM can be an excellent choice if you plan to move or refinance before the five-year fixed period ends, as it typically offers a lower starting rate than fixed-rate loans.

Q3: How often does a 7/6 ARM adjust?

A 7/6 ARM features a fixed interest rate for the first seven years, after which the rate adjusts every six months for the remainder of the loan term.

Q4: Can I refinance my ARM into a fixed-rate mortgage?

Yes, many homeowners use a rate-and-term refinance to convert their adjustable-rate mortgage into a fixed-rate loan before their initial fixed period expires.

Q5: What does a lifetime cap mean on an ARM?

A lifetime cap is a consumer protection feature that strictly limits the maximum interest rate you can be charged over the entire life of your adjustable-rate mortgage.