Understanding the Basics of a Conventional Mortgage

If you are looking to buy a home in Dunedin, FL, a conventional mortgage is often the most popular financing choice. A conventional fixed-rate mortgage offers stability and predictability, ensuring your principal and interest payments remain exactly the same throughout the life of the loan. Whether you are a first-time homebuyer or looking to upgrade to a larger property, understanding how a conventional loan works is essential to making a sound financial decision.

Unlike government-backed loans, conventional mortgages are originated and serviced by private lenders. Because they are not insured by the federal government, they typically require a solid credit score and a reliable income history. Many borrowers opt for a 30-year fixed-rate mortgage to keep their monthly payments affordable and budget-friendly over the long term. If you already have a quote from another lender, remember that we are experts at providing second opinions on conventional mortgages to ensure you get the absolute best terms available.

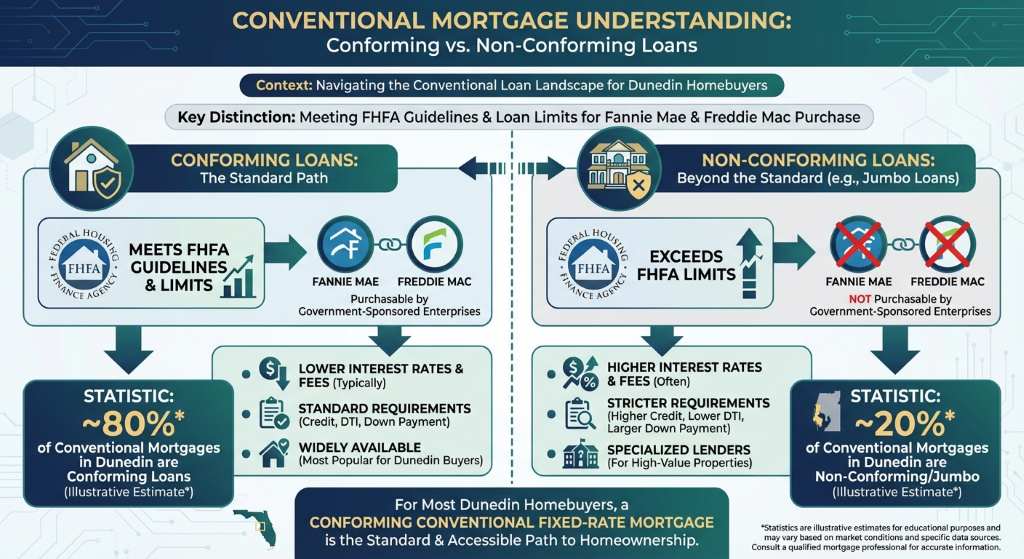

Conforming vs. Non-Conforming Conventional Loans

When exploring a conventional mortgage, it is crucial to understand the difference between conforming and non-conforming loans. A conforming loan meets the specific guidelines and loan limits set by the Federal Housing Finance Agency (FHFA), allowing it to be purchased by Fannie Mae or Freddie Mac. For most homebuyers in Dunedin, a conforming conventional fixed-rate mortgage is the standard path to homeownership.

- Conforming Loans: These loans adhere to standard loan limits and typically offer highly competitive interest rates. They are ideal for buyers with good credit and a steady income.

- Non-Conforming Loans: These loans exceed the FHFA loan limits or do not meet standard credit guidelines. The most common type of non-conforming loan is a jumbo mortgage, which is necessary for purchasing luxury properties or homes in high-cost areas.

If a conventional loan does not fit your current financial profile, you might want to explore government-backed alternatives like an FHA purchase loan, which often has more flexible credit and down payment requirements.

| Feature | Conforming Conventional Mortgage | Non-Conforming (Jumbo) Mortgage |

|---|---|---|

| Loan Limits | Adheres to FHFA county limits | Exceeds FHFA county limits |

| Credit Score Requirement | Typically 620 or higher | Usually requires 700 or higher |

| Down Payment | As low as 3% for first-time buyers | Typically 10% to 20% or more |

| Interest Rates | Generally lower and highly competitive | Slightly higher due to increased lender risk |

Why Choose Us for Your Conventional Mortgage in Dunedin

Securing a conventional mortgage does not have to be a stressful process. As a trusted local mortgage loan consultant in Dunedin, FL, Sean McManamon and his team are dedicated to helping you turn your homeownership dream into reality. We guide you through every step of the loan process, from the initial strategy consultation call to pre-approval, underwriting, and final closing. Our local loan officers are passionate about helping you find the perfect mortgage that suits your specific needs.

We know that finding the right loan option is critical for your financial future. That is why we are experts at providing second opinions on conventional mortgages. If you are unsure about the rate or terms another lender offered, let us review your scenario. With our streamlined process, you can complete our secure application in just 12 minutes. Let us provide the personalized service and competitive rates you deserve.

Q1: What is a conventional mortgage?

A conventional mortgage is a home loan that is not insured or guaranteed by the federal government. It is offered by private lenders and typically requires a good credit score and a stable income.

Q2: How much down payment is required for a conventional fixed-rate mortgage?

While many people believe a 20 percent down payment is required, first-time homebuyers can often qualify for a conventional loan with as little as 3 percent down.

Q3: What is the difference between a conforming and a non-conforming loan?

A conforming loan stays within the loan limits set by the FHFA and meets Fannie Mae or Freddie Mac guidelines. A non-conforming loan, such as a jumbo loan, exceeds these limits and usually requires stricter credit criteria.

Q4: Can I get a second opinion on my conventional mortgage offer?

Absolutely. We highly recommend getting a second opinion to ensure you are receiving the best possible interest rate and terms. We specialize in reviewing conventional mortgage offers to help you save money.

Q5: How does my credit score impact a conventional mortgage?

Your credit score plays a significant role in determining your interest rate and eligibility. A higher credit score generally unlocks lower interest rates and better loan terms for a conventional fixed-rate mortgage.

Ready to Secure Your Conventional Mortgage?

Apply Now in Just 12 MinutesOr call Sean McManamon at 1-727-639-5968 or email sean@mortgagesbysean.com for a free strategy consultation!