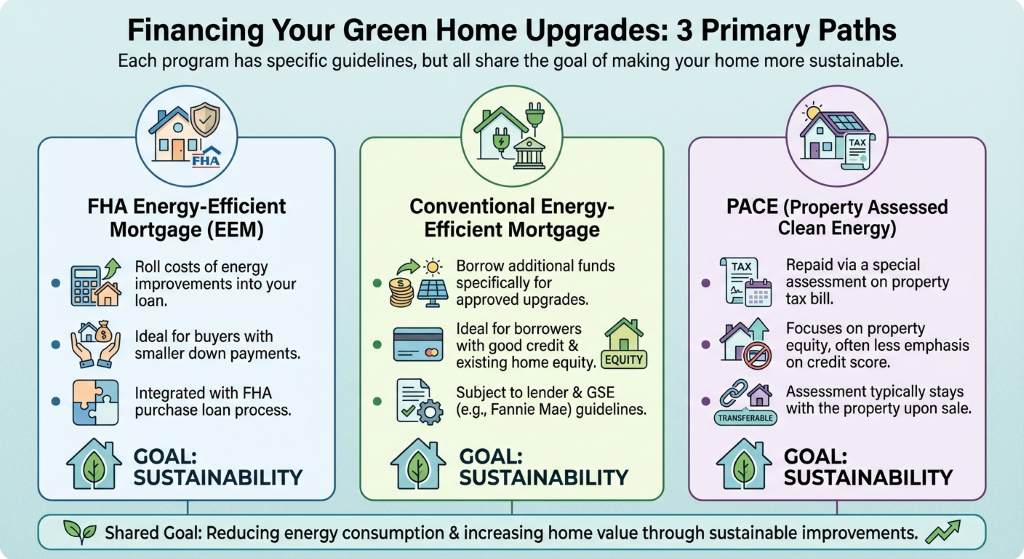

What is an Energy-Efficient Mortgage (Green Mortgage)?

Are you looking to buy a home in Dunedin, FL, but want to make sure it is as eco-friendly and cost-effective as possible? An Energy-Efficient Mortgage, also known as a Green Mortgage, might be the perfect solution. This unique financing option allows homebuyers and current homeowners to finance the cost of adding energy-efficient improvements into their new or existing mortgage.

By upgrading items like solar panels, HVAC systems, or double-pane windows, you can lower your monthly utility bills and increase the overall comfort of your home. Whether you are exploring a conventional fixed rate mortgage or another loan type, we are experts at providing second opinions on energy-efficient mortgages to ensure you get the best possible terms.

Types of Energy-Efficient Mortgages: FHA, VA, and Conventional

When it comes to financing your green home upgrades, there are three primary paths you can take. Each program has specific guidelines, but all share the goal of making your home more sustainable.

- FHA EEM: The Federal Housing Administration offers a fantastic program for buyers who might not have a massive down payment. An FHA Energy-Efficient Mortgage allows you to roll the costs of energy improvements into your loan. If you are already considering an FHA purchase loan, adding the EEM feature is a seamless way to upgrade your property.

- VA EEM: Available exclusively to eligible veterans and active duty service members, the VA Energy-Efficient Mortgage lets you add up to $6,000 to your loan amount for approved energy improvements. It is a great way to maximize your VA benefits while reducing your carbon footprint.

- Conventional EEM: Supported by Fannie Mae and Freddie Mac, a Conventional Energy-Efficient Mortgage is ideal for borrowers with stronger credit scores. These loans often provide higher limits for energy upgrades and can be applied to both home purchases and refinances.

Working with a local mortgage loan consultant like Sean McManamon ensures you navigate these options smoothly and find the exact fit for your Dunedin home.

| Loan Type | Down Payment Requirement | Max Energy Improvement Amount | Best For |

|---|---|---|---|

| FHA EEM | As low as 3.5% | Up to 5% of property value (limits apply) | First-time buyers & moderate credit |

| VA EEM | 0% (for eligible veterans) | Up to $6,000 (standard) | Veterans & active military |

| Conventional EEM | As low as 3% to 5% | Up to 15% of the as completed appraised value | Borrowers with strong credit profiles |

How to Qualify and Apply for Your Green Mortgage

Securing an energy efficient mortgage involves a few extra steps compared to a standard home loan, but the long-term savings are well worth the effort. To qualify, lenders typically require a Home Energy Rating System (HERS) report. An approved energy rater will inspect the property and detail the recommended upgrades, their costs, and the projected energy savings.

Here is a quick overview of the process:

- Schedule an Energy Assessment: Hire a qualified professional to evaluate the home.

- Choose Your Upgrades: Decide which improvements make the most financial sense based on the assessment.

- Submit Your Application: Provide the energy report to your lender along with your standard mortgage documents.

Because the projected energy savings can be used to help you qualify for a larger loan amount, an energy efficient mortgage actually increases your buying power. If you are unsure where to start, reach out to Sean McManamon to review your specific scenario.

Q1: What is an Energy-Efficient Mortgage?

It is a specialized loan that allows borrowers to finance energy-saving home improvements as part of their primary mortgage, rather than taking out a separate, higher-interest loan.

Q2: Can I use an EEM for an existing home?

Yes, you can use an energy efficient mortgage to refinance your current home and pay for upgrades like new insulation, solar panels, or a high-efficiency HVAC system.

Q3: Do I need a perfect credit score to get a Green Mortgage?

No. Programs like the FHA EEM cater to borrowers with lower credit scores, while Conventional EEMs are available for those with stronger credit profiles.

Q4: What types of improvements are covered?

Eligible improvements generally include weatherization, solar water heaters, double-pane windows, and high-efficiency heating and cooling systems. The upgrades must be proven to save money on energy bills.

Q5: Why should I get a second opinion on my EEM?

Guidelines for green mortgages can be complex. Getting a second opinion ensures your lender is maximizing your eligible improvement funds and offering the most competitive interest rates available.