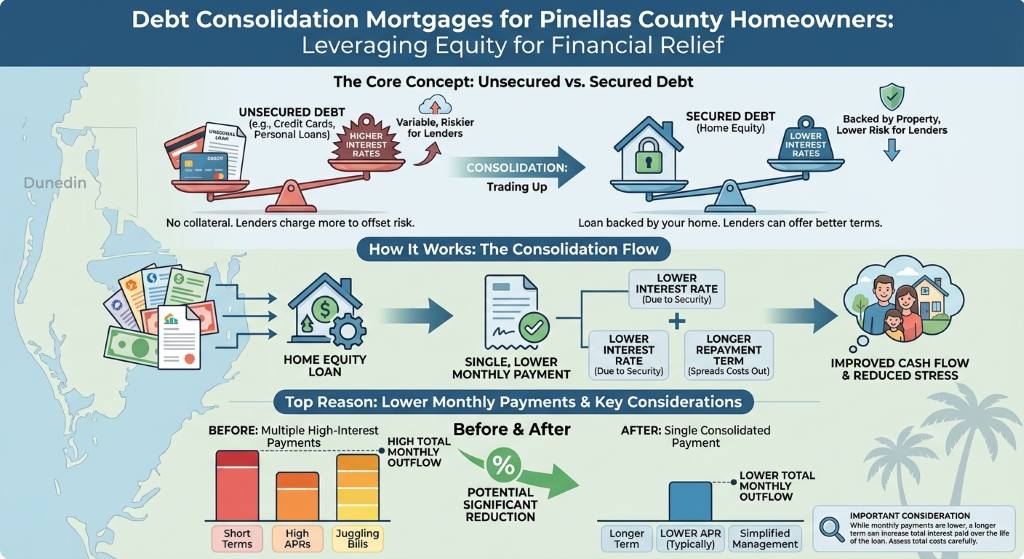

What is a Debt-Consolidation Mortgage?

If you are feeling overwhelmed by high interest credit cards, personal loans, or medical bills, a debt consolidation mortgage might be the perfect solution to regain control of your finances. Also commonly referred to as a debt consolidation loan, this financial strategy allows homeowners in Dunedin, FL, to roll multiple high interest debts into a single, more manageable monthly mortgage payment.

At Mortgage Info by Sean, led by Sean McManamon, we specialize in helping Florida residents navigate their debt consolidation options. By leveraging the equity you have built in your home, you can potentially lower your overall interest rate and simplify your life. There are a few primary ways to achieve this:

- Cash Out Refinance: This replaces your existing mortgage with a new one for a higher amount than you currently owe. You receive the difference in cash, which you can use to pay off other debts. Learn more about a cash out refinance.

- Home Equity Loan or Second Mortgage: This allows you to borrow a lump sum against your home equity without touching your primary mortgage rate. Discover if a home equity loan second mortgage is right for you.

We are experts at providing second opinions on debt consolidation mortgages. If you have already received a quote from another lender, let us review it to ensure you are getting the best possible terms for your unique situation.

Why Choose a Debt Consolidation Loan in Florida?

Many homeowners in Dunedin and across Pinellas County are discovering the powerful benefits of a debt consolidation loan. When you consolidate debt using your home equity, you are essentially trading unsecured debt for secured debt. Because the loan is backed by your property, lenders can typically offer significantly lower interest rates.

Here are some of the top reasons to consider a debt consolidation mortgage:

- Lower Monthly Payments: Spreading your debt over a longer term and securing a lower interest rate can drastically reduce your monthly financial obligations.

- Simplified Finances: Instead of juggling multiple due dates and minimum payments, you only have to worry about one single payment each month.

- Potential Tax Benefits: In some specific cases, the interest paid on a mortgage may be tax deductible. It is highly recommended to consult with a tax advisor regarding your specific situation.

- Improved Credit Score Potential: Paying off maxed out credit cards can lower your credit utilization ratio, which is a major factor in determining your credit score.

However, it is crucial to remember that a debt consolidation mortgage requires discipline. Once those credit card balances are at zero, you must avoid running them back up. Sean McManamon is dedicated to helping you build a sustainable strategy to ensure long term success.

| Debt Type | Average Interest Rate | Typical Repayment Term | Monthly Payment Impact |

|---|---|---|---|

| Credit Cards | 20% to 25% | Revolving | High and Variable |

| Personal Loans | 10% to 15% | 2 to 5 Years | Moderate to High |

| Debt Consolidation Mortgage | 6% to 8% | 15 to 30 Years | Low and Predictable |

How to Apply for a Debt Consolidation Mortgage in Dunedin

Getting started on your debt consolidation journey is easier than you might think. Our streamlined loan process at Mortgage Info by Sean is designed to get you from application to closing with minimal stress.

Here is how our all-in-one solution works:

- Strategy Consultation: Schedule your strategy consultation call with our experts today. We will review your current debts, evaluate your home equity, and determine if a debt consolidation mortgage is your most advantageous route.

- Pre-Approval: Getting pre-approved ensures a seamless process. We will look at your credit score, debt to income ratio, and employment history.

- Start Your Application: You can complete our secure application in just 12 minutes to take the first official step toward your loan.

- Loan Processing and Underwriting: We gather all required documents. Our underwriting team carefully reviews the entire loan package to ensure accuracy and compliance.

- Closing: Once approved, documents are sent to a local Dunedin title company to finalize your new debt consolidation loan.

Remember, we are experts at providing second opinions on debt consolidation mortgages. Do not settle for the first offer you receive without letting our local team verify that it is truly the best fit for your home ownership and financial goals.

Q1: What are the basic requirements to qualify for a debt consolidation mortgage?

To qualify, lenders typically look at factors such as your credit score, income, employment history, debt-to-income ratio (DTI), and the amount of equity available in your home.

Q2: Can I use a cash-out refinance to consolidate my debt?

Yes, a cash-out refinance is one of the most common debt consolidation options. It allows you to replace your current mortgage with a larger one, taking the difference in cash to pay off high-interest bills.

Q3: How does my credit score affect my debt consolidation loan approval?

Your credit score impacts your loan eligibility, interest rate, and terms. Higher credit scores generally qualify for lower interest rates, maximizing the savings you get from consolidating your debt.

Q4: What is the difference between a fixed-rate and an adjustable-rate mortgage for consolidation?

A fixed-rate mortgage has a constant interest rate and monthly payments for the entire loan term, providing stability. An adjustable-rate mortgage (ARM) has a lower initial rate but can change periodically based on market conditions.

Q5: What are the closing costs associated with a debt consolidation mortgage?

Closing costs are fees associated with finalizing your mortgage, including appraisal, title insurance, and lender fees. They typically range from 2% to 5% of the loan amount, but these can often be rolled into the loan balance.